RCM Fundamentals

Introduction

- Harnessing the Power of Numbers!

- Innovation – Collaboration – Leadership

- Connecting to the College’s ERP Strategy

- A College-built Approach

- Project Phases

- RCM Glossary

About Responsibility Center Management

- What is Responsibility Center Management?

- RCM Principles

- RCM Best Practices

- Stewardship and Entrepreneurial Thinking

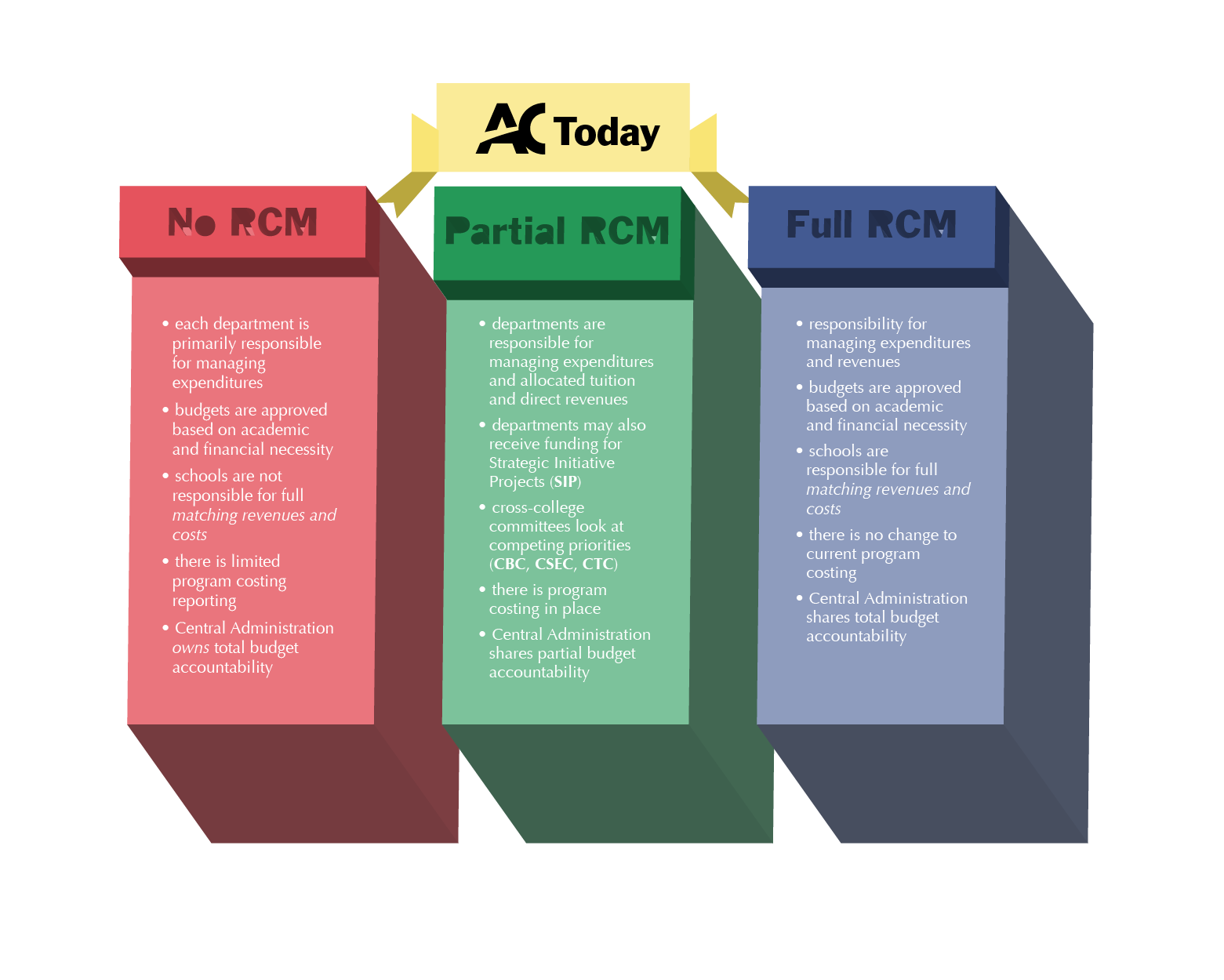

RCM at a Glance: Algonquin, Today and Tomorrow

Budget Principles and Financial Sustainability

About Allocations

About Revenues

About Expenditures

What is the Total Cost of Ownership?

Standardized Units of Exchange

Cost-Sharing Resources

What is LEAN Management?

Support Tools: Algonquin’s ERP Business Transformation Strategy

Sample Scenarios

About the “Made at Algonquin” RCM Model

RCM Fundamentals

Introduction

Harnessing the Power of Numbers!

Did you know that Algonquin College operates with an annual budget of $300 million to serve more than 20,000 fulltime and 37,000 part-time students? We employ nearly 4,000 faculty and staff to deliver 167 postsecondary programs plus a roster of apprenticeship, career and college preparation, continuing education, and corporate training programs.

Responsibility Center Management (RCM) empowers academic and administrative units to manage their own resources within the framework of a unified institutional vision. RCM stewardship is expected to play a key role across the College in every program by supporting decentralized governance and fiscal management, inspiring 360° views to budget optimization, and igniting innovative and entrepreneurial initiatives.

Innovation – Collaboration – Leadership

The RCM Project will advance Algonquin’s leadership in strategic resource allocation by undertaking a consultative and comprehensive review of the current financial processes and RCM models in other academic institutions, in order to deliver a “best practices” blueprint.

With the development of Strategic Recommendations and an Action Plan, the RCM Project will foster the alignment of Algonquin’s delivery of academic excellence with its commitment to financial sustainability.

Connected to the College’s ERP Strategy to Transform Business Processes

RCM is being carefully planned in close consultation with the College’s Enterprise Resource Planning (ERP) Business Transformation Strategy. ERP is the technical term for a suite of core business management software, usually a suite of applications. ERP facilitates information flow between all business functions, and manages connections to internal and external stakeholders.

Business services comprise a wide range of functions such as attracting and recruiting prospective students, faculty and funders, managing student records, managing human resources and day-to-day accounting operations. These services run more efficiently when they can be linked together by a software platform that is easy for students and staff to use.

In this way, the user-directed, self-service capacities of ERP underpin the shift toward the department-level RCM business model: the systems needed to manage budgets and resources autonomously will be in place just as departmental managers and staff are ready to work with them to direct their own academic or non-academic activities.

A College-built Approach

Algonquin College will undertake the Responsibility Center Management (RCM) Project with the goal of strategically aligning revenues and expenditures within the College to better align its resource allocation to institutional priorities in accordance with the Vision, Mission, Core Values, and Strategic Plan.

This project will involve a comprehensive, inclusive review of the current budget and financial reporting system, external review of RCM models in other academic institutions, and present options for costing allocations relevant to the requirements of the College. In addition, the project will include communication and training plans. The RCM Project will culminate with the development of recommendations and an action plan to achieve the goal of aligning academic authority with resource allocation while incenting College leaders to maintain and improve College financial sustainability. As part of the implementation, a series of business process reviews will be undertaken to ensure that impacts to students, faculty, staff, volunteers and external clients at all levels are supported through communication and training.

The RCM Project (2014-2016) will advance Algonquin’s leadership in strategic resource allocation by undertaking a consultative and comprehensive review of the current financial processes and RCM models in other academic institutions in order to deliver a “best practices” blueprint.

With the development of Strategic Recommendations and an Implementation Plan, the RCM Project will foster the alignment of Algonquin’s delivery of academic excellence with its commitment to financial sustainability.

At present, the College centrally manages most revenues and expenditure, allotting specific budgets to academic and administrative managers to cover program costs. However, RCM principles are already in practice within specific units.

Ancillary Services (including Food Services, Retail Services, The Print Shop, Card Services, Parking & Locker Services and Conferences Services) now incorporates unit-performance budgeting procedures similar those adopted by the University of Toronto RCM budgeting framework. The Centre for Continuing and Online Learning (CCOL) has also implemented a budget model that capitalizes on innovation, entrepreneurial activities, applicant demand, and market forces for launching new programs on a cost-recovery basis. In this way, CCOL is a prime example of RCM principles that balance academic entrepreneurship with fiscal responsibility.

Project Phases

Click image to enlarge

RCM Glossary

Hold Harmless Principle

The timeframe in which there will be no deficit repayment under RCM, defined under the RCM Principles as a two-year period. No school or department will be penalized financially by the move to RCM within this two-year period.

“One Common Basket of Services”

All “Non-Academic” departments at Algonquin College which support the “Academic” departments. Some examples are Finance & Administrative Services, ITS and Human Resources.

Under RCM, the costs of these supporting departments are allocated to the Academic departments in totality. The Academic departments cannot pick and choose what they pay for – they have access to all Non-academic services.

Materiality

The materiality principle states that there is a financial level which is set based on the net impact of doing so has such a small impact on the financial statements that a reader of the financial statements would not be misled.

A materiality level is set for any accounting or budget principle to minimize time spent on a level of detail which does not add value to the overall process or statement under review.

At Algonquin for RCM, we are assuming that the materiality level is 1% of Total Revenues. Anything under this 1% is considered not material.

Subvention

Subvention funding is a small portion of the total Provincial funding grants held by the College to be distributed to the Academic departments to help them achieve their stretch contribution margins or targets, during the Hold Harmless period.

In future years, the goal is that the Academic departments will be able to achieve their stretch targets without the use of subvention funds.

About Responsibility Center Management

What is RCM?

“Institutions that consider adopting a form of Responsibility Center Management (RCM) often make the mistake of thinking they are simply changing the way they budget income and expense, when in fact they are fundamentally changing governance and management relationships across the institution.”

Dr. Robert Zemsky

Thinking about RCM for Algonquin College (2013)

The Learning Alliance for Higher Education, University of Pennsylvania

In an RCM system, each individual school within the college is said to earn its own income— principally tuitions, program fees, and research and other grants and contracts—and these funds in fact belong to the schools.

Each school also receives a central allotment, usually defined as a subvention, which, combined with its own income, represents the funds a given school has to pursue its academic agenda. The revenue that a school earns belongs to that school, whose responsibility it is to decide how those funds are spent based on its own priorities.

An agreed-upon part of that income is returned to the Central Administration in the form of allocated cost charges equal to each school’s fair share of central administrative costs and the cost of operating and maintaining the facilities each school uses. The central administration establishes guidelines and limits for each category of expense, but not allocations per se.

This decentralized approach is attractive to many higher education institutions as a way to stimulate entrepreneurial thinking around attracting students and funders, and to improve efficiencies in response to tight fiscal conditions according to each department’s values and priorities.

Click image to enlarge

RCM Principles

Click image to enlarge

RCM Best Practices

Leadership

RCM works best with strong deans and strong senior management: dynamic tension is necessary to match the will of the part with the way of the whole

Good numbers make good neighbours: transparency and integrity in data promotes understanding of the internal economics of relative budget profiles

RCM presidents needs sufficient and liquid subvention resources (rainy days) and surge tanks (bumper crops)

Senior leadership is required to monitor that trade barriers and enrolment grabbing between schools do not impede the integrity of the College and its programs

RCM needs a resident intellectual champion

The Commons

RCM cannot be made perfect by extensive and prevaricative debate or by continually refining the algorithms and rules

Holding and advancing the commons requires active and aggressive leaders

Central service providers need incentives to be efficient

Responsibility Centers

The real wins in RCM come from proper exercise of the pie-expanding incentives rather than from rearranging rules to claim other center’s money

Entrepreneurial systems do not necessarily create entrepreneurs

RCM deans need professional financial officers

RCM promotes the engagement of faculty and staff in the quantification and implementation of the plan they help formulate: this involvement yields a more robust organization that is more adaptable in the face of exogenous change

Supplemental assistance from the common fund is not an entitlement: it is awarded to neutralize a exceptional revenue/cost mismatch; to plan for success; to advance institution-wide goals; to fuel promising startup ventures

RCM encourages provision of efficient and competitive administrative services

Measure and manage administrative services in both central units and responsibility centers to avoid duplication (e.g. through outsourcing)

About Allocations

Under the RCM model, allocations refer to the methodology to apportion the revenues to the academic schools and the expenses for services delivered by non-academic units as a shared common services pool. As Algonquin College transitions from partial to full RCM, a custom-built model depends on key decisions pertaining to these allocations.

Revenue: Provincial Grant Allocation

The recommended allocation of the provincial grant is in the 40%-50% range. Schools would realize this portion of the provincial grant as revenue earned. This allows all academic departments to have a transparent proportional allocation based on the value of Weighted Funding Units (outside of Dean’s control) and budgeting enrollment (within Dean’s control). This allows academic departments to have some part of grant before subvention fund, a small number will break even or have small surplus. The allocation amount can grow over time as departments move to optimize resources and the subvention fund shrinks.

Expenses: Allocation for Central Administrative Costs (excluding Physical Resources)

The allocation for central administrative costs would be based on a percentage of direct costs. This method is simple and transparent, allowing one common basket of services for one price. This formula is easy to apply universally and allows Deans to focus on academic priorities.

The definition of the basket of services offered by each non-academic department would be governed by a Service Level Agreement (SLA). SLAs will define services provided by non-academic departments to all college departments but specifically provide Deans with metrics on services provided as an accountability value-for-money measure. Any service offered exclusively between non-academic departments would be included in the SLA so noted.

In accounting, the term “materiality” refers to the role of information if its omission, duplication or misstatement could influence economic decisions. Materiality will have to be addressed when working with rural campuses and ancillary units to ensure they are not double-charged for services (such as operating satellite libraries, health services and bookstores apart from the main services offered at Woodroffe Campus). Where duplication of services exists, respective parties should be encouraged to locate collaborative operating efficiencies in order that all departments contribute to the commons fairly.

For non-academic departments, allocated net costs will exclude physical resources costs. Therefore, the contribution margin allocated for separately for physical resources would represent a deficit (overhead) that would be managed as part of the directors’ total costs and services delivery rather than charged back to the academic departments.

All departments would be required to opt in and agreements can be modified over time if justification is provided showing duplication of services within a department.

Expenses: Allocation for Physical Resources

The cost allocation for physical resources will be based on real, measurable usable space per department (non-academic, academic and ancillary). This percentage promotes fairness regardless of building occupied and allows all departments to have a transparent allocation based on their space within their control.

This method incentivizes all departments to optimize space utilization, noting that Physical Resources plans to upgrade their tracking software by Spring 2015 to enable more precise metrics and real time changes for Ministry reporting, eliminating the need for point in time data (currently being used).

Both Overhead and Woodroffe support would be governed by a Service Level Agreement:

- Overhead component (Directors office, Planning, Engineering, OHS, etc.): Shared by all departments by total usable square footage, including rural campuses and leased premises.

- Woodroffe operating costs: Shared by all departments at Woodroffe based only on the usable square footage at Woodroffe.

Again, materiality will have to be addressed when working with rural campuses and ancillary units to ensure they are not double-charged for services but operate within a materiality limit reflecting the needs of the entire institution.

About Revenues

Provincial Grants

- Grant allocation to be assigned to schools based on WFU’s X budgeted enrollment

- Variance reporting to be done based on variance to budget

- % of grant allocated – not 100% still to be determined – (90% for F15/16 Model)

- “Holdback” would go to balance schools, fund new opportunities or contingencies

- Provincial Grants represent the largest single source of College funding and the General Purpose Operating Grant (GPOG) and the Growth Grant are the core operating grants distributed to the College.

- The distribution of the GPOG to the Schools is based on the Weighted Funding Units calculated for each School and the value assigned to the WFU by the Ministry

- The grant is paid using a “Three year Average with Two Year Slip”.

Tuition and Other Fees

- Based on the number of students and the specific tuition earned by each program within each Academic Department.

- Academic Department keeps all revenue earned through tuition of their programs.

- Incidental Fees earned by Academic Department – Fees collected from enrolled students for materials consumed as part of the program delivery.

- International Student Premium – Academic Department receives 35% of International Student Premium.

Other Sources of Revenue

- Revenues earned through services offered by programs within a department (Restaurant International – School of Hospitality, Dental Clinic – School of Health, Public Services and Community Studies)

- Contract revenues earned by department

About Expenses

Salaries

- Faculty, Administrative and Support staff salaries employed within department.

- Actual payroll costs of full and part-time employees.

- Includes all fringe benefits associated with employees.

Space Costs

|

General Overhead (All Campuses) |

Woodroffe Specific |

|

|

- Per square foot assignable allocation used

Central Administration Charges

- 18 departments (excludes Ancillary, International & Physical Resources)

- Direct costs are salaries & costs already charged to Academic departments

- Controllable at Dean level

- Allocated in one pool to Academic departments based on budgeted total direct costs

Other Program Costs

- Direct operating costs of department – office or instructional supplies, printing, etc.

- Contracted expenses, professional development, travel, etc.

About Service Level Agreements (SLAs)

As Algonquin College transitions from partial to full RCM, agreements between service providing units and service receiving units will be created as useful tools to identify and confirm expectations on both sides.

The Service Level Agreements (SLAs) will explicitly define the goods and services to be provided in exchange for a share of the central administrative allocation pool. SLAs are based on a simple and transparent formula: one common basket of services for one price.

These formal contracts eliminate any potential confusion by allowing Deans to control the scope of services they wish to contract, and Directors to define the goods and services to be provided. One SLA per department or area will be negotiated, which may be reviewed annually with formal renegotiation after 5 years.

The SLAs define key elements:

- The scope of work for both core and ad hoc services;

- The benchmarks for core and ad hoc service provision, either current or industry standards;

- The timeframes for service delivery: for instance, a help-desk ticket response from ITS within two business days, or an expense report processed by Finance within 10 business days;

- The metrics by which the provision of goods and services will be measured: performance tracking should be simple and meaningful;

- The procedure for dispute resolution in the event of a problem between the parties; and

- Duties and responsibilities applicable to both parties

Academic Departments

- Ottawa Valley campuses

- Algonquin Heritage Institute

- Faculty of Arts, Media & Design

- Faculty of Health, Public Safety & Community Studies

- Language Institute

- Faculty of Construction, Technology & Trades

- School of Business

- School of Hospitality & Tourism

- Center for Continuing & On-line Learning

- Corporate Training

Central Administrative

- Academic Operations

- Academic Development

- Advancement

- Applied Research

- Business Development

- Community Partnerships

- Finance & Admin

- Foundation

- Human Resources

Space

- Physical Resources

- Information Technology Services

- International

- Learning & Teaching Services

- Registrar’s Office

- Student Support Services

- Workplace & Personal Development

- Office of President, BOG

- Office of VPA

Ancillary

- not part of shared costs

Sample Scenarios

Collaborating, not Competing

Program A offers a valuable training program for professional certification, and markets the course to corporate clients (business to business). Eventually, it is decided that this training should be part of the curriculum in Program B (business to customer).

Over time, the training program becomes heavily subscribed by Program B students, and reduces the demand from Program A corporate clients. A and B begin to dispute the territory for this training program and the matter goes before the Dean.

The Program A corporate sales manager feels she has “lost” sales; however, the net effect of the increasing popularity of the training program in Program B has resulted in a 200% increase in revenue for the College.

The Dean persuades A and B to work together to streamline their offerings, by sharing the pool of qualified instructors and the costs for classroom space, thus bringing the cost down, and by proportionally realizing revenues based on their respective client bases.

RESULT:

- Best practice service delivery for same program

- More revenue to College

Reaching out to the Community

A regional campus has dedicated space facilities suitable for corporate meetings and special events. The campus pays for the total cost of operating the space, even though it is used only about 20% of the time, for periodic daytime meetings.

Working with RCM principles, the Director decides to make overtures to the local community to seek groups who might make use of the space during its vacant periods for a small stipend. Agreements are created with several organizations, bringing the use of the facility up to 80% and significantly defraying the operating costs of the space.

The small extra charge to cover administration and maintenance of the space is offset by increased parking and food services revenues from extra visitors to the campus.

RESULT:

- Community awareness of College facilities & programs for future student recruitment

- Inexpensive marketing tool

- Cost recovery of facilities expenses

- Increased revenue opportunities for Ancillary services

Reducing Duplication

A certain collaborative software is licensed by the College’s Information Technology Services, who maintains tech support during weekday daytime hours.

Program C requires the same software, primarily for evening and international time zone activities. The program decides to purchase a separate (duplicate) license in order to get vendor-supplied 24/7 tech support.

Under RCM, Program C could negotiate with ITS to use the software under the existing ITS licensing agreement, and cost-share its portion of the additional tech support coverage required.

RESULT:

- Decreased Direct costs to Program C

- Simplified ITS network by standardizing to one software application – cost savings on duplicate software may offset increased costs to support 24/7

- Increased service to all academic departments

About the “Made at Algonquin” RCM Model

Learn more about the “Made at Algonquin” RCM model here. A guide to the RCM Model, built for Algonquin College.

Documenting and Journalizing Under RCM

RCM Fundamentals

Learn More About Implementing RCM at Your Institution

A two-part webinar presentation explores the principles of RCM and considerations for implementing this model on your campus.

Larry Goldstein (Campus Strategies, LLC) covers:

- Determining whether RCM is the right fit for your institution

- Assessing whether your institution is ready to implement RCM

- A review of issues associated with the RCM model

- Key considerations for an implementation timeline

- Case study examples: successful and unsuccessful examples of moving to RCM

RCM Fundamentals

- Webinar slides: Part 1 RCM Fundamentals part 1

- Webinar slides: Part 2 RCM Fundamentals part 2